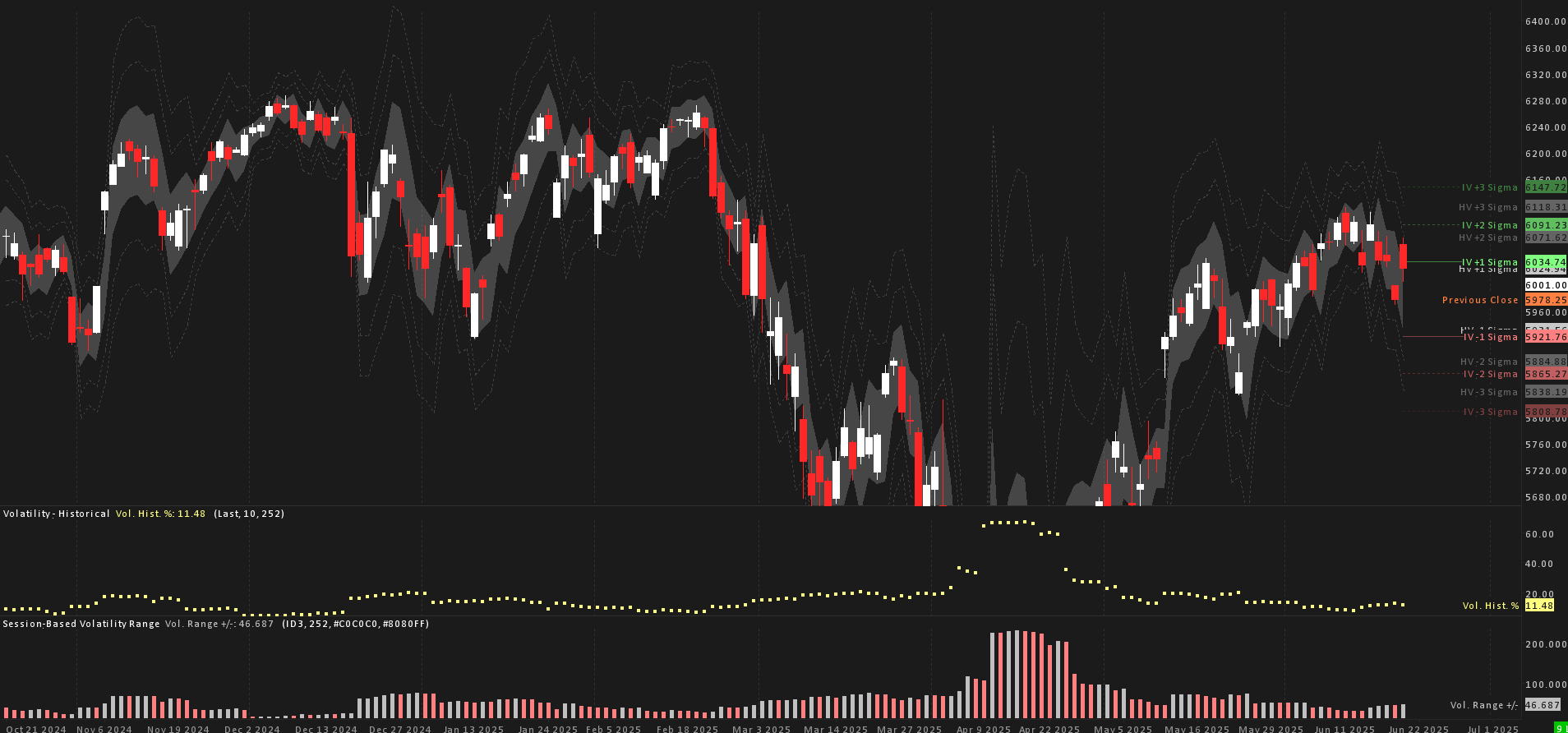

OverviewStatistically expected price ranges.

This custom Sierra Chart study provides a volatility-based framework to project

expected price movement using ±1σ, ±2σ and ±3σ ranges. The levels

are calculated from either Historical Volatility (HV) or Implied Volatility (IV) and plotted directly

on the chart, giving you a clear, quantitative reference for where price is statistically expected to

remain.

It alerts when price breaches the ±1σ levels and tracks how often price

closes inside the ±1σ HV range, so you carry a containment statistic for backtesting and

probability modeling.

Volatility modesHistorical or implied.

01Historical Volatility Mode (HV)

Translates HV % values from Sierra Chart's built-in “Volatility - Historical” study into

projected price ranges.

- References Sierra Chart's built-in Volatility - Historical study.

- Projects price ranges based on annualized HV.

- Alerts on HV ±1σ breaches.

- Tracks the % of bars historically closing inside HV ±1σ (analytics output).

02Implied Volatility Mode (IV)

Accepts a manual IV % input to overlay sigma-level forecasts from externally sourced Implied

Volatility, useful for traders pulling IV from options chains.

- Manual IV % input.

- Uses the same sigma logic for projecting IV-based ranges.

- Plots separate overlays for IV projections.

- Alerting support for IV ±1σ crossings.

The formulaHow the sigma ranges are built.

The same sigma projection formula is applied independently for both HV and IV:

±σ range = Previous Close ± (Volatility × √(ForecastBars / BarsPerYear)) × Price

- Volatility is either HV or IV.

- ForecastBars is the user-defined horizon (1 bar = a 1-day projection).

- BarsPerYear reflects the trading calendar (252 for daily charts).

- PreviousClose is the close of the previous bar.

This yields statistically scaled ±1σ, ±2σ and ±3σ

price boundaries around the previous close.

How to useRead the guardrails.

-

±1σ ≈ 68% containment. Under normal-distribution assumptions, about 68%

of closes stay within ±1σ.

-

Not a mean-reversion signal. Price will not necessarily revert when it touches a sigma

level. Treat the boundaries as probabilistic guardrails: crossing them stacks the odds against

further expansion unless confirmed by context.

-

Manage risk and exits. Use the sigma levels to scale out, manage risk, or confirm

potential exhaustion, especially with no high-impact catalysts in play.

-

Use with market context. Strongest in confluence with order flow, volume clusters,

market structure, or known catalysts like news and reports.

-

Backtesting analytics. The built-in analytics summary calculates how often price closed

inside ±1σ historically, useful for backtesting and probability modeling.

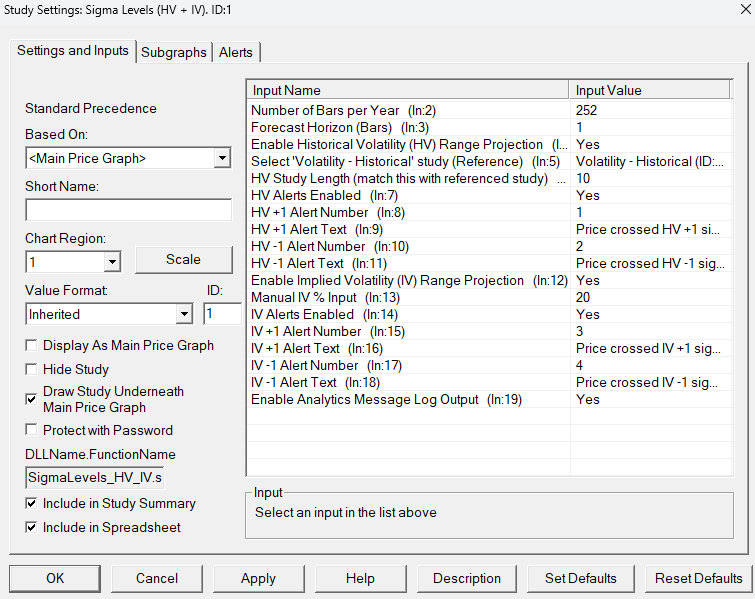

Every element configurableStudy settings

Good to knowFAQ.

How do I get access after subscribing?

At checkout you provide your Sierra Chart Account Name (Help → About →

Account Name / Username). Within 24 hours we add you to the list of users authorized to use the

study. Restart Sierra Chart and open the automatically downloaded chartbook.

Is there a free trial?

Yes - both subscription plans (monthly and annual) start with a 7-day free trial:

you won't be charged until the trial ends, and you can cancel anytime before then. The lifetime

plan is a one-time purchase, so there's no trial.

Can I use the indicator on all symbols?

Yes. Just be sure to adjust the session times when switching to other symbols.